-

Publish Your Research/Review Articles in our High Quality Journal for just USD $99*+Taxes( *T&C Apply)

Offer Ends On

Publish Your Research/Review Articles in our High Quality Journal for just USD $99*+Taxes( *T&C Apply)

Offer Ends On

Gideon Mukui*

Corresponding Author: Gideon Mukui, School of Economics, University of Nairobi, Kenya.

Received: May 26, 2026 ; Revised: June 02, 2026 ; Accepted: June 08, 2026 ; Available Online: June 11, 2026

Citation:

Copyrights:

Views & Citations

Likes & Shares

The paper uses a double deficit model that stresses two constraints: inadequate domestic savings and inadequate foreign currency. In the analysis, the government makes decisions on foreign borrowing and taxation while the households choose how much money to consume and save. In this case the decision is made in two steps: first, the government chooses whether to borrow money from abroad, and then households adjust their saving behavior. The ARDL model was used to analyze the data. The results showed that foreign debt had a negative effect on domestic savings in the short run and appositive effect in the long run. The findings also indicated that foreign debt has negative effect on capital accumulation both in the short run and in the long run as predicted by the theoretical model. Based on the findings, this study therefore, recommends a reduction in the external borrowing. This is poised to minimize the negative short run impact of debt in the economy. In the same vein, the study recommends debt to be used in productive investment to generate returns to repay the principle and the interest accrued thereby boosting economy-wide savings in the long run. A prudent use of debt would also boost the economy’s capital accumulation which is a catalyst for economic growth thus generating additional resources for debt repayment other development needs.

Key words: Domestic savings, foreign debt, fixed capital formation, private consumption.

INTRODUCTION

Public debt is important because it helps government undertake huge public projects with generational benefits. However rapid and high levels of public debt adversely affect the economy. Developing countries have heavily relied on international capital inflow to finance development projects because it offers an opportunity for them to grow and protect themselves against shocks but at the expense of rising debt levels. By contrast, domestic factors such as inflation and increasing fiscal deficits as well as external factors among them declining commodity prices and unfavorable terms of trade, and international interest rate, continue to worsen. The unfavorable economic conditions have resulted in most of the economies accumulating a huge public debt stock thereby increasing the burden of debt service despite the numerous efforts to contain the problem(Okafor & Tyrowicz, 2010).

Economic theory posits that debt should be used in productive investment with a potential to generate returns for repaying the debt. This means that prudent use of borrowed resources can spur economic growth and improve living standards. However, high levels of debt beyond certain threshold could have negative effects in the economy. For example, a rise in government borrowing from the domestic market could potentially lead to crowding out of the private investment. Similarly, foreign borrowing could impact the economy negatively due to a rise in interest payment arising from exchange rate depreciation and other international shocks. The increase in debt repayment level consumes considerable amounts of domestic resources which could have been otherwise invested back into the economy. Aggregate demand would also be affected if the government resorts to increased taxation to raise the necessary revenue required to finance government expenditure and to repay the previous loans. This will in turn leave consumers with limited resources at their disposal for consumption and savings (Blackmon, 2014).

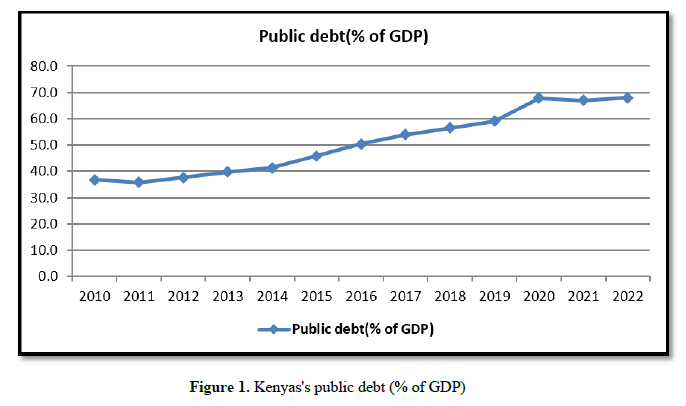

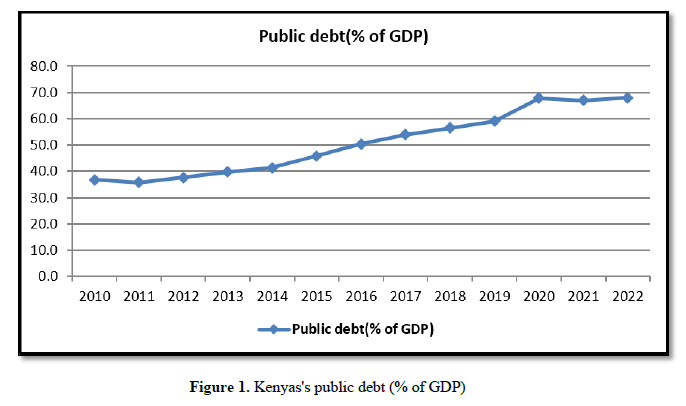

The pace of public debt accumulation in Kenya has increased substantially in recent years, raising concerns among policymakers about debt crisis. The recent trend shows that Kenya hastaken up more debt upwards. The country has been unable to constrain the growth of public debt and ensure that sufficient revenue remains available to finance other important development and recurrent expenditures after debt service payments. Figure 1 provides a glimpse of Kenya’s debt as a percentage of GDP.

The ongoing increase in Kenya's debt levels has raised serious questions about the sustainability of the country's debt, and organizations like the World Bank and the International Monetary Fund (IMF) have emphasized the importance of Kenya focusing on fiscal consolidation. Total public debt as of December 2022 was Kshs 10.3 trillion 67.9% of GDP, above the IMF's recommended limit of 50.0% for developing nations by 17.90% points. Additionally, the debt service to revenue ratio was 47.9%, 17.9% percentage points higher than the IMF's suggested limit of 30.0%, underscoring the burden that public debt payment has on the nation's spending. The steep depreciation of the shilling has continued to increase pressure on the government as the majority of the external debt is denominated in USD. The high depreciation of the shilling has continued to put more pressure on the debt serving. Due to the emphasis on both development and recurrent expenses, the budget deficit has averaged 8.1% during the past ten years which has led to rising debt levels. Other notable factors that have contributed to rising debt stock are slow growth in revenue receipts amidst growing government expenditure and reduction in exports earnings.

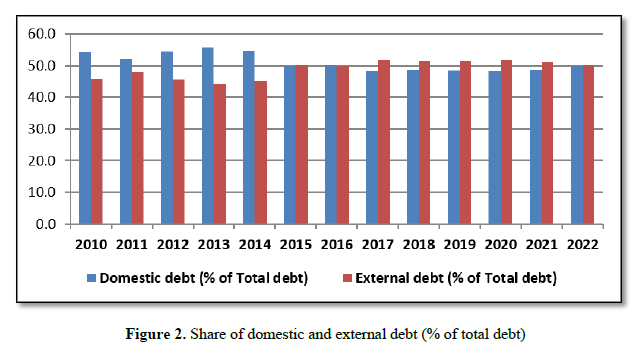

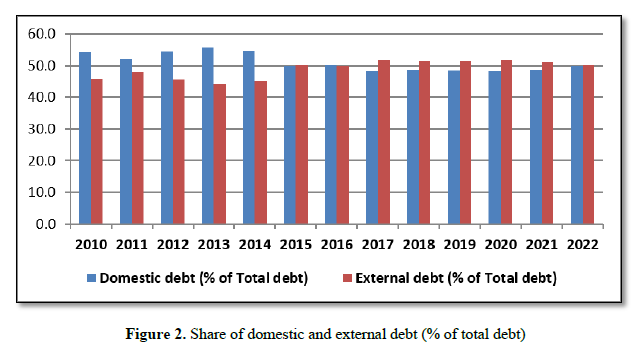

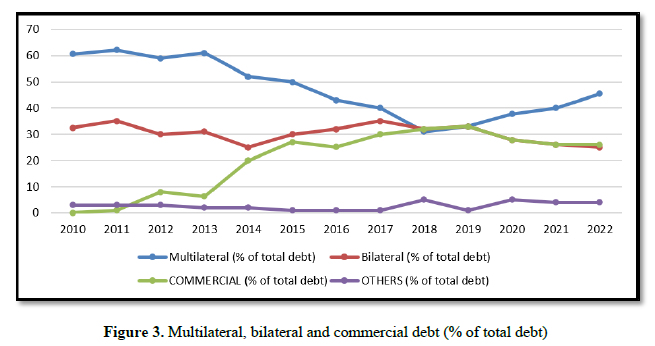

The composition of the public debt has also changed significantly in terms of both domestic and foreign debt as shown in Figure 2.

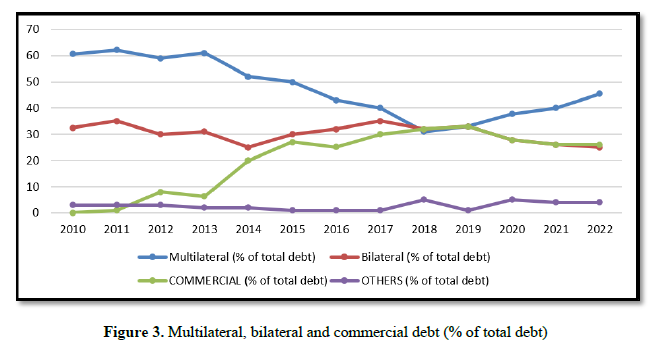

Kenya had an increase in its exposure to bilateral and multilateral loans in FY'2021/2022, which can be attributed to the favorable terms granted in terms of low interest rates and extended payback times. In particular, the cost of Eurobonds (commercial borrowing) increased due to higher interest rates on the global financial market in FY'2021/2022. This was caused by the increased perception of risk brought on by economic uncertainty, which was brought on by increased global inflationary pressures and increased worries about the sustainability of debt in the majority of developing countries. This led to an increase in bilateral and multilateral loans from 33.1% in 2019 to 45.4% in 2022 while during the same period, commercial decreased from 33% to 26.2%.

The increase in public debt and in particular foreign borrowing has raised debt servicing costs and concerns over debt rescheduling. These concerns were confirmed by Debt Sustainability Analysis report conducted jointly by IMF and World Bank in January 2022. The DSA established that the ratings for debt distress remained high. The report further noted that debt distress was caused by high deficits from the past which was aggravated by the current shock combined with the sharp slowdown in export and economic growth in 2020 caused by the COVID-19 pandemic. The shocks resulted in deterioration of solvency and liquidity debt indicators.

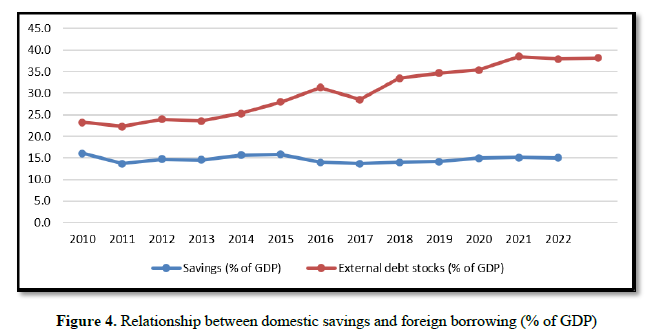

An increase in foreign borrowing leads to a reduction in national savings and investment, which further lead to decreases in future income. This would be the case because low savings or rather savings constraints play a significant role in pushing countries to indebtedness. (Tiruneh, 2004) argued that the economic reason why countries resort to borrowing, whether domestic or external is due to an increase in the gap between national savings and domestic investment. Domestic savings are an important prerequisite for capital formation and growth because they finance capital stock in the long –run (Freytag, 2013).

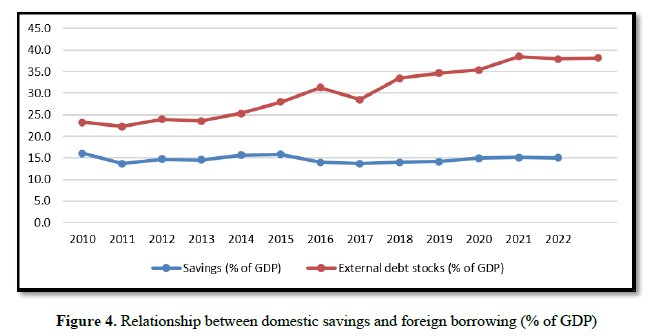

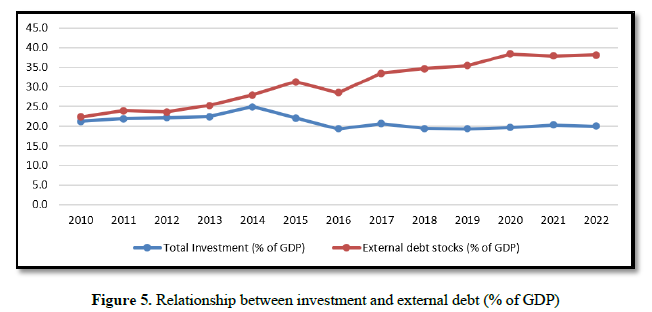

Economic literature documents that there is an association between domestic savings and foreign borrowing. Feldstein (1982) postulated that external debt can be used to finance capital stock in the short and medium term but domestic savings have to rise in the long-term to repay the debt. Root (1990) on the other hand argued that growth and development is mainly constrained by the vicious cycle of the saving-investment gap which signify inability to save sufficient amounts of resources to finance the desired level of investment and foster self-sustained economic growth. This is brought about by increases in repayment of external borrowing at the expense of domestic savings. Figure 4 gives an overview on the relationship between foreign borrowing and domestic savings in Kenya.

The decline in savings is partly be attributed to high levels of foreign borrowing which imposes additional tax measures to cater for interest payment on debt thereby affecting the propensity to save and invest. Thus, it is imperative that any analysis of the effect of public debt must consider its impact on national savings and capital formation.

Empirical literature on public debt focuses more on its effects on economic growth. It is important, however, to note that the economic growth effects of public debt occur through other channels such as savings and investment which are likely to decline due to the increases in interest payment on debt. Previous studies fail to acknowledge that the effect of public debt in the economy depends on how it affects individuals’ propensity to save and invest due to the increases in taxes to repay the debt. This research paper therefore, enriches the existing research to fill this gap by investigating how government foreign borrowing influences domestic saving behavior and investment. The remainder of this paper is organized as follows: Section 2 provides the literature review while section 3 explains the data, variables and methods used in the analysis. Section 4 gives the empirical results and discussion while section 5. Provides conclusion and policy implications.

LITERATURE REVIEW

The burden of debt service has continued to increase despite numerous efforts at addressing the problem. The increase in debt service burden in Kenya is one of the motivating factors that has ignited our interest in attempting to ascertain the linkage between foreign debt and domestic savings. Froning and Schavey (2000) observed that debt servicing burden may end consuming greater shares of revenue and scarce foreign resources. This is because as debt servicing costs increases countries must allocate a considerable share of their budgets to servicing their debt, which may result in higher taxes, more borrowing, and the risk of default. Theory on the macroeconomic effects of government debt is generally diverse and to some extend there exist divided opinions regarding its impact on the economy. The conventional view held by most economists and policymakers is that in the short run public debt stimulates aggregate demand and economic growth but crowds out capital and reduces national income in the long run. Another view based on Ricardian equivalence hypothesis (RIH) argues that government choice between tax and debt financing of government deficits is irrelevant. Equivalence theorem views public debt as economically neutral: that is, it does not matter whether the government finance budget through taxation or issuing interest bearing bonds since both will reduce the current period consumption.

Barro (1974) supported the theory arguing that if there is tax cut and bond is issued household will save enough to cover expected high tax in future to pay for both interest and the principle. Keynesian theory of public debt views public debt as a kind of capital inflow of which government can leverage on and raise funds to finance productive projects hence increase national income (GDP). This theory assumes that public debts are maintained at levels where it impacts economic growth positively. Threshold theory unlike Keynesian theory appreciates that despite the fact that public debt boosts investments and accelerates economic growth, these benefits cease beyond some levels of debt and sets in negative impact on economy through a reduction of investment. This occurs due to higher distortionary tax rate on capital aimed to raise resources to service the debt hence causing cause capital flight. Crowding out theory asserts that accumulation of debt has effects on investment through the resource mechanism concept (Cohen, 1993).

Diamond (1965) notes that internal and external debt may affect savings in two main ways, which arises due to the taxes needed to finance interest payments. According to diamond, taxes directly reduce lifetime consumption available to individual taxpayer. Moreover, by reducing his disposable income, taxes reduce his savings and hence the capital stock. However, the impact of internal debt on savings due to reduction in the capital stock arising from the substitution of government debt for physical capital in individuals’ portfolios.

According to Griffin and Enos (1999) external flow such as aid and debt would limit domestic savings. However, if the cost of aid or the rate of interest on foreign loans is less than the incremental out-put capital ratio, it will be helpful for a country to borrow as much as possible and augment domestic savings. In light of this, and given a target rate of growth of a country, foreign capital will lead to higher consumption and domestic savings will just be a residual representing the difference between desired investment and the amount of foreign capital available.

Weale (2009) while examining the burden on national debt postulated that in a situation where national debt displaces investment in the produced capital then high levels of debt will lead to a reduction in the country’s future income which in turn causes national saving to decline due to interest payment on debt. By comparing the share of national savings as a proportion of GDP with the current budget deficit, which is equivalent to current government de-saving, the authors argued that increasing government current deficit by one unit reduces national savings by 0.5 units. Cohen (1993) on the other hand postulated that it is not the stock of public debt that directly impacts on private investment but rather debt servicing that may reduce public investment-thereby impacting on private capital accumulation through complimentary effect on savings.

According to Tiruneh (2004), the gap between domestic investment and national savings is related to the economic the tendency to borrow externally. Similar to this, Root (1990) argued that the vicious circle of the savings-investment gap is the major obstacle to the growth and development of emerging economies. This limitations on savings indicates developing nations such as Kenya are unable to save sufficient resources to carry out the desired level of investment, which could result in self-sustaining growth. Foreign borrowing may also be considered as foreign savings, which would then fill the gap generated by low domestic savings.

Numerous studies have been conducted to determine how foreign debt affects investment and economic growth. However, there appears to be a gap in the literature on foreign debt, though, in that an analysis of the problem of how foreign debt affects domestic savings has not been explored. Using time series data from 1976 to 2015, Jawaid and Saleem (2017) analyzed the relationship between foreign capital inflows and economic growth in Pakistan by employing Johansen Cointegration technique and OLS. The study considered external debt and foreign direct investment (FDI) among other international capital flows. The finding from the Cointegration test indicated external debt and FDI had significant long run relationship with economic growth. On the other hand, the OLS regression results showed the effect of FDI on economic growth was negative and significant while external debt had positive and significant effect on GDP growth.

Akram (2016) investigated whether public debt influenced pro-poor growth from South Asian Countries. The study aimed at examining the consequence of public debt on economic growth and its linkage to poverty in Bangladesh, India, Pakistan, and Sri Lanka using panel data for the period 1975-2010. To conduct the analysis, Two Stage Least Square (2SLS) and GMM estimation methods were used. The finding of the empirical study showed that total public debt had negative impact on economic growth. The findings also revealed that the external debt and external debt servicing had no significant effect on income inequality. However, domestic debt had positive impact on economic growth and inversely related with the GINI coefficient implying internal debt is pro-poor compared to external borrowing.

Hayford (2005) used structural vector auto regression (VAR) model to analyze the impact of fiscal policy on national savings in United States (US). Specifically, the study incorporated measures of fiscal policy to estimate the dynamic impact of fiscal policy shocks on output gap and national savings. It was evident from the finding that positive shocks to government purchases and negative shocks to real net taxes increased output gap. The results further showed that national savings increased marginally as a result of positive shocks to the government’s structural surpluses. In addition, positive shocks to government consumption expenditure reduces national savings while negative shocks to real net tax revenues as a share of GDP had small negative impact on national savings.

Islam and Biswas (2005) investigated public debt management and debt sustainability in Bangladesh using evolution of public debt as the theoretical framework. They tested total debt dynamics using the debt dynamics equations from Ley (2003). They used the data sample for the period 1981- 2006. The findings revealed that growth in debt-GDP ratio did not pose any serious concern on stability of fiscal policy. The result further indicated the debt-dynamics turned more favorable during 2001-2006 compared with the 1980s. In addition, the primary deficit and domestic debt-to GDP ratio on average, declined to 2.70 per cent and 49.52 per cent respectively.

Mahmood et al (2009) investigated public and external debt sustainability in Pakistan for the period1970- to 2000. The study relied on a method used by Papadopoulos and Sidiropoulos (1999) to ascertain public debt and fiscal sustainability conditions. They found that on the side of external debt sustainability analysis, primary current balances played a significant role in contributing to the rise in external debt ratios. Additionally, interest rate factor was marginally responsible for contributing towards the rise in debt to GDP ratio in 1990s and 2000s and the levels of public debt and external debt indicators have been far from the debt sustainability levels since the last three decades.

Makin (2005) investigated public debt sustainability and its macroeconomic implications in Indonesia, Malaysia, Thailand, and the Philippines (ASEAN-4). The study employed a method for assessing fiscal effort required to stabilize or lower debt-GDP ratio. The study found that for large primary surpluses of between 15 and 20 per cent of GDP, the fiscal policy required to drastically lower public debt would obviously be infeasible within a five-year time-frame. Giver the underlying economic conditions at that time and if the central governments of Indonesia and Thailand ran primary surpluses averaging around 5 per cent of GDP, the 25 per cent target would be reached within a decade.

Nyongesa, et al. (2013) examined the sustainability of the current account deficits in Kenya between 1970 to 2012 using stationarity and Cointegration test. The findings indicated that Current account was stationary at levels implying that it is reverting and temporary but external debt was finite and sustainable. The results suggested that exports and imports were cointegrated with the cointegrating coefficient of 0.21989 which was not significant. The implication was that current account was not on the sustainable path therefore indicating a weak form of sustainability.

Osuka and Chioma (2014) analyzed the impact of budget deficits on macro-economic variables in the Nigerian economy between 1981 and 2012. Specifically, the study sought to investigate long-run relationship between budget deficits and other macro-economic variables in Nigeria. The resulted the result indicated existence of long run relationship existed. The study however found that the test for causality showed that there exists no causality between deficits and interest rate, budget deficits and inflation and budget deficit and nominal exchange rate. These results further indicated that budget deficits exert significant impact on the macroeconomic performance of the Nigerian economy.

It is evident from the literature review that most of the authors focused on the effect of total debt economic growth (Jawaid and Saleem, 2017; Akram, 2016; Osuka and Chioma, 2014; Islam and Biswas, 2005). The empirical studies examining the impact of government borrowing on national savings is scarce with only two studies reviewed so far (eg; Okafor and Tyrowicz, 2009; Hayford, 2005). Further, previous studies are mostly cross-sectional (Okafor and Tyrowicz, 20019), which fails to account for cross-country differences such as institutional development. In addition, the methodology used in the previous studies are not robust enough to provide convincing results. For example, Jawaid and Saleem (2017) used OLS while Hayford (2005) used structural vector auto regression (VAR) to analyse the data. The novelty of the present study is that we inquire as to the link between domestic savings and foreign debt using a dynamic model involving the government and a representative household. The study also applies Autoregressive Distributed Lag (ARDL) model which is a robust methodology to analyze the data.

METHODOLOGY

Theoretical Model

In this study, we use a continuous two-period economy endowed with capital. This framework of modelling foreign debt follows money in the utility function (MIU) postulated by Sidrauski (1967) and refined by Walsh (2003). The model is a two-stage game between the government's borrowing efforts and the representative household's adjustment of its savings effort. In this framework, we assume that both the government and the household derive utility from the consumption and the flow of services financed with the external borrowing . The demand for infrastructure services is always positive.

Assuming that the government is the social planner and that it takes into account the rational expectations of its economic agent, the utility function is stated as;

,

,

Where is the flow of services yielded through infrastructure projects that have been financed by external borrowing while yields utility directly. In both arguments, utility is assumed to be increasing, strictly concave, and continuously differentiable. The demand for infrastructure services is always positive if we assume that

By taking into account the rational expectations of households, the government is viewed to be taking paths for foreign borrowing. The representative household chooses consumption paths subject to budget constraints specified in total utility as;

equation 1 shows notions of the utility provided by infrastructure services financed by foreign borrowing in addition to utility derived from consumption of goods and services. If the marginal utility from infrastructure services is positive, then the equation implies that by holding the path of real consumption constant for all t, the utility of the individual is increased by an increase in the flow of infrastructure services financed by foreign borrowing.

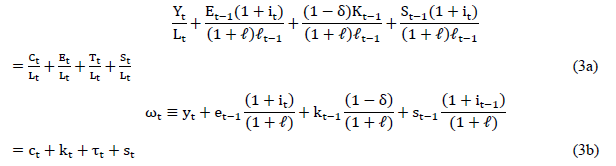

To complete the specification of the model, we assume that the rational economic agents in this case the representative household can earn interest rate on savings. Output is produced using physical capital according to the standard neoclassical production function. The representative household allocates its resources between consumption, gross investment in physical capital, and gross domestic savings based on its current income, its assets, and the government's policies about borrowing from abroad.

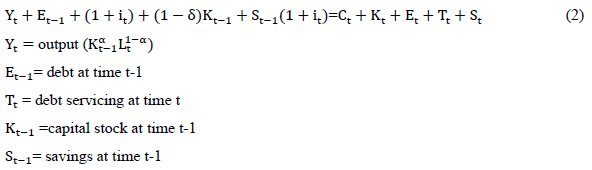

If the depreciation rate is , the aggregate budget constraint for the economy takes the form

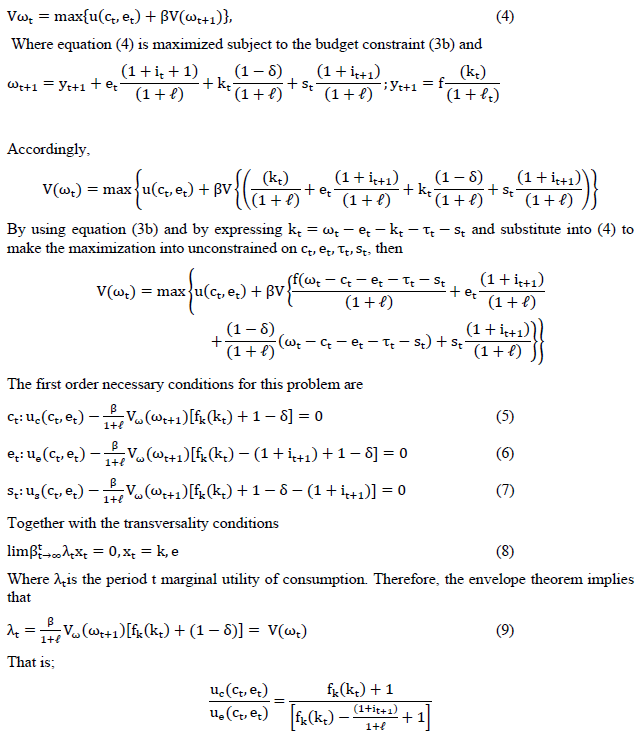

Equation (3a) represents standard identity transformed to account for per capita terms. Each agents owns certain amount of capital stock or assets, the initial at time zero. In our analysis, consumption cannot exceed earnings and inflows whether foreign or domestic. Taking into account the representative household rational expectations, the problem of the government is to choose the paths of and . The representative household chooses taking into account the decisions of the government. Both the household and the government maximize equation (1) subject to equation (3b). since this problem represents a dynamic optimization, we formulate the problem in terms of the value function. The justification for this is that the value function gives the maximized value of the utility that the representative household and the government can achieve by behaving optimally given their current state. The representative agent’s initial resources is is the stated variable for the problem. The value function, defined as the present discounted value of utility, if the agents optimally choose consumption, capital holdings, savings, and foreign borrowing, is given by:

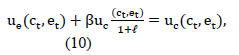

The interpretation of the first-order conditions is very clear. Because resources must be divided between consumption, foreign borrowing and savings, each must yield the same marginal utility when allocated optimum. Using equation (5), (6), (7) and (9), this can be written as

which states that the marginal benefit of additional foreign borrowing at time t must equal marginal utility of consumption at time t. Similarly, Equation (5) for capital holdings implies that net marginal return from additional capital holdings must equal the marginal utility from consumption. Equation (6) for foreign debt implies that the net marginal benefit of capital holdings, augmented by benefits enjoyed from services rendered by the means of foreign borrowing, must equal the net marginal benefit of foreign borrowing. Equation (7) for savings implies that net marginal return from capital holdings, augmented by interest earned via domestic savings, must equal net marginal benefits from domestic savings. Equations (5) to (7), together with budget constraints (3), characterize the government’s decisions regarding foreign borrowing and the representative household’s adjustment of its domestic savings behavior at each point in time. Equilibrium also requires that the demand for infrastructure services provided by means of foreign borrowing equals the supply of foreign borrowing by the government (which is assumed to be exogenous).

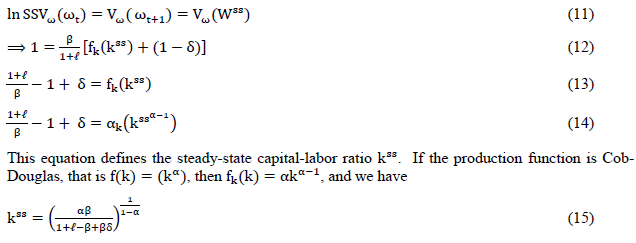

Steady-state equilibrium

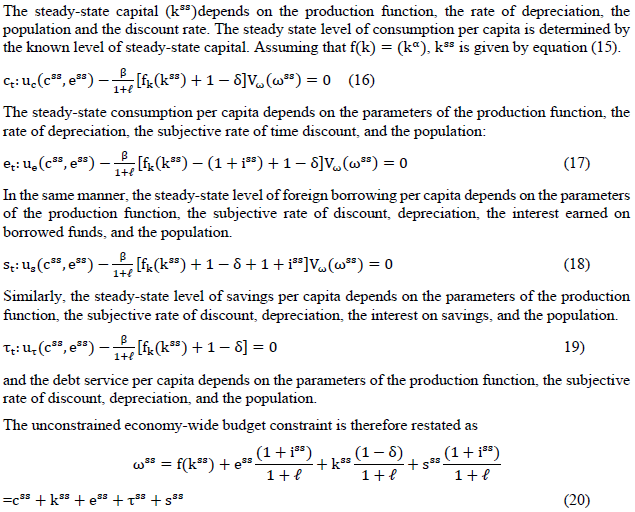

Setting the population growth rate at rate we now investigate the steady-state equilibrium of the economy. The evaluated steady-state equilibrium values are denoted by superscript . The steady-state values of consumption and savings must satisfy the necessary first-order conditions for the government, the representative household’s decision problem, the economy-wide budget constraint, and the specification of the exogenous rate of foreign borrowing and debt service. These conditions can be written as

Our interest is the savings behavior of the representative household in response to foreign borrowing. Therefore, solving the steady-state gross domestic savings we have

Definition, measurement of the variables and methods of analysis

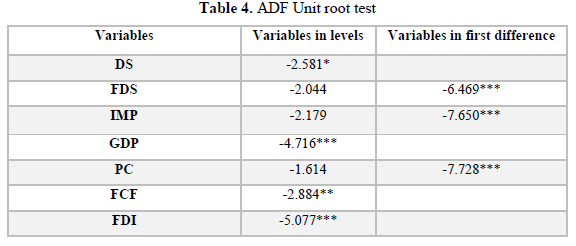

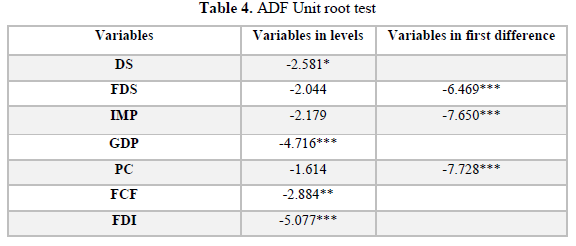

In this study, a time series data for the period 1980 to 2023 was used analyze the results. The data was sourced from World Bank development indicators. The choice of the sample period was guided by the availability of adequate time series spanning forty-three (43) years suitable for time series analysis. The key variables of interest are domestic savings and foreign debt service. The choice of the two main variables is based on the assumption that foreign debt service depletes the available financial resources for domestic investment and savings. However, domestic savings is also affected by other factors such as the level of economic growth, imports, private consumption, FDI and fixed capital formation. These variables were, therefore, included in the analysis because of the varied ways in which they affect domestic savings. The data was analyzed using ARDL model because it is suitable for analysing a mix of I(0) and I(I) variables as indicated in Table 4 for Unit root test.

RESULTS

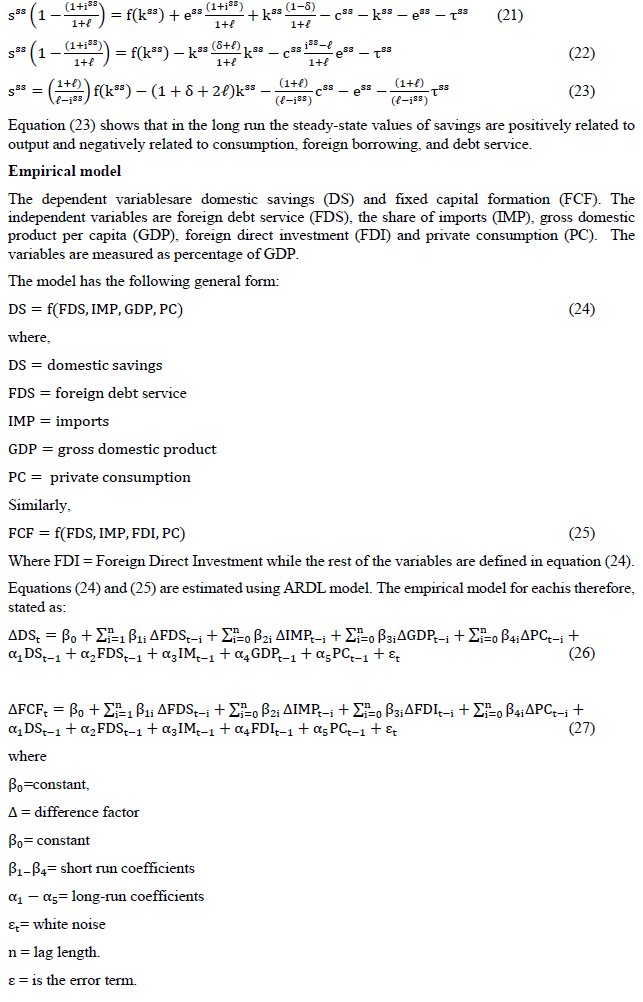

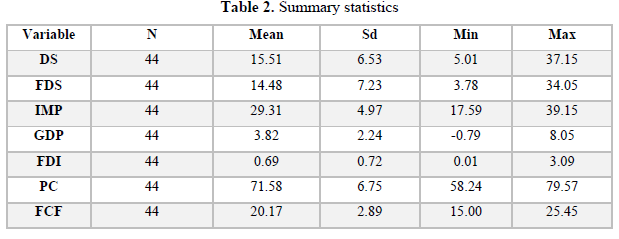

Table 2 displays descriptive statistics of the variables indicating that the mean value for domestic savings as 15.51 while mean value for foreign debt service is 14.48. The minimum values these variables are 5.01 and 3.78 while the maximum values are 37.15 and 34.05 respectively. The descriptive statistics show a close relationship in the behavior of domestic savings and foreign debt

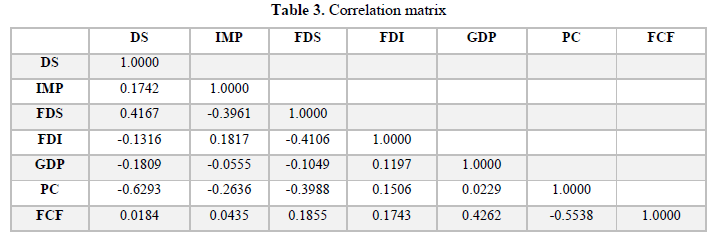

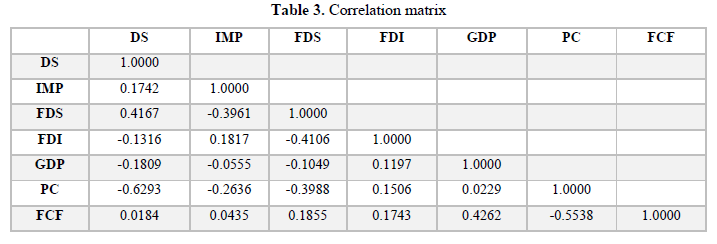

Table 2 shows absence of multicollinearity among the variables.

The results show that domestic savings and real GDP variables are I (0) since they are stationary in levels while foreign debt service, imports and private consumption variables are I(I)since they become stationary in the first difference.

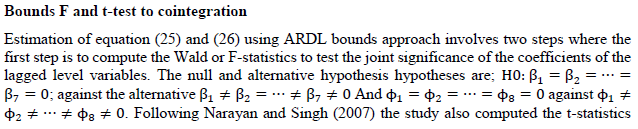

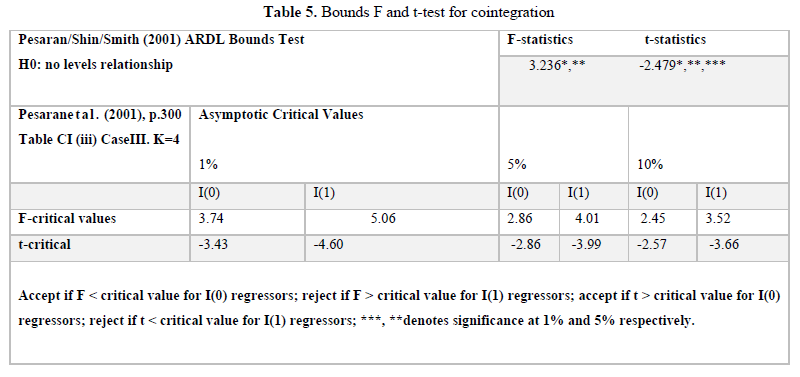

The results in Table 5 show that the null hypothesis of no level relationship is rejected since the calculated F-statistic is greater than the critical values for I (0) regressors at 10% and 5% respectively. Again, when using the t-statistics, the null hypothesis is rejected since the calculated t-statistic is less than the critical value at 10% ,5% and 1% levels for I (0) regressors.

Diagnostics

Durbin-Watson d-statistic (15, 36) = 2.485029

Ramsey RESET F (3, 18) = 0.4143

Prob > F = 0.9370

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity: chi2(1) = 0.11

Prob >ch2 =0.7367

Source: Author’s own computation using stata; **p<0.05,*p<0.1

Standard errors in parentheses.

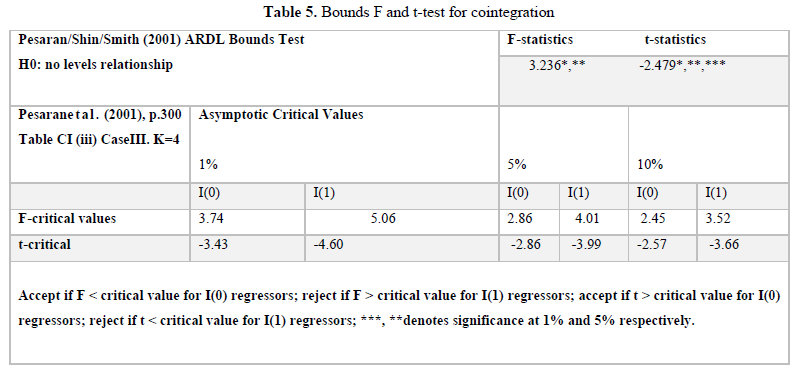

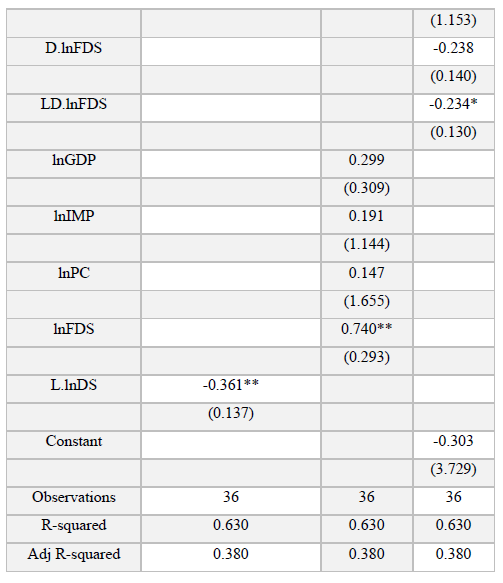

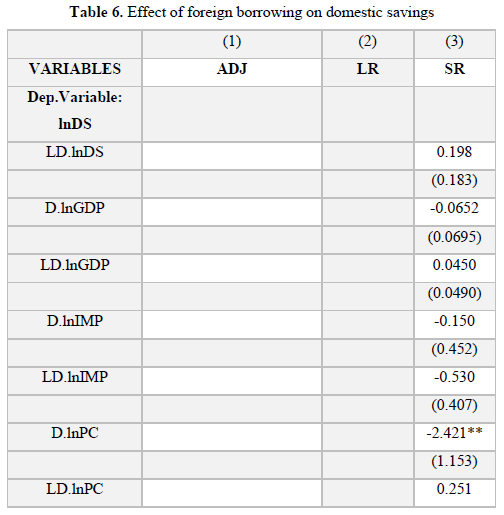

The short run results in table 6 show that foreign debt service and private consumption have negative effect on domestic savings. This is confirmed by the coefficients of foreign debt servicing and household consumption variables that are significant at 5% and 10% respectively. A unit increase in servicing foreign debt and household consumption expenditure reduce domestic savings by 0.2 and 2 units respectively. The first difference of GDP has a negative but insignificant effect on savings while the first lag of GDP is positive but also insignificant.

In the long run, GDP, imports and household consumption have positive but insignificant effect on savings while foreign debt service has a positive effect on savings. A unit increase in servicing foreign debt raises domestic savings by 0.7 units ceteris paribus. The long run results for the GDP are consistent with the theoretical model prediction that in the long run a rise in economic growth will lead to an increase in domestic savings. Similarly, the short run results for the foreign debt servicing and household consumption are consistent with the theoretical model prediction that in the long run, an increase in debt servicing and consumption expenditure leads to a decline in domestic savings. The error correction term (ECM-1) is significant at 5% implying a moderate speed of adjustment to equilibrium at 36% in the event of shock to the system. All the post-estimation tests in table 5 show the model is free from serial correction as given by the Durbin Watson statistics, and the residual have a constant variance as given by the Breusch-Pagan / Cook-Weisberg test for heteroskedasticity. The Ramsey reset test shows the model has no omitted variable.

Diagnostics

Durbin-Watson d-statistic (9, 40) = 2.016464

Breusch-Godfrey LM test for autocorrelation chi2= 0.122

Prob ch2>=0.7268

Ramsey RESET F(3, 28) = 0.4143

Prob > F = 0.2018

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity: chi2(1) = 1.50

Prob >ch2 = 0.2212

Source: Author’s own computation using stata; *p<0.01

Standard errors in parentheses.

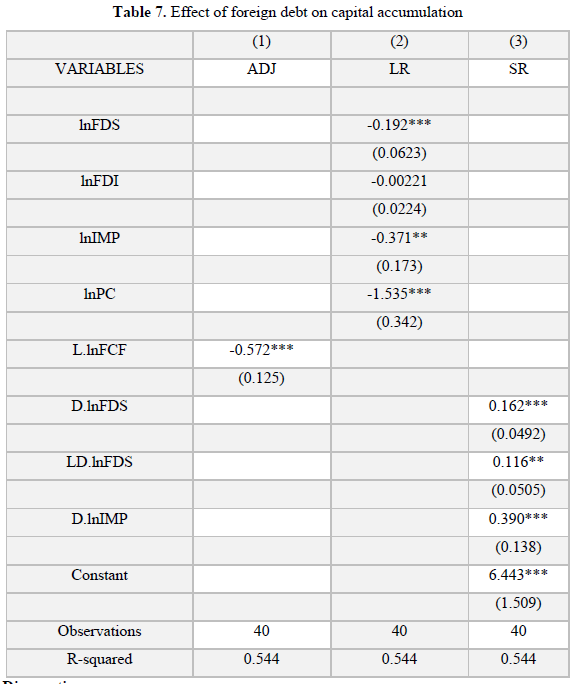

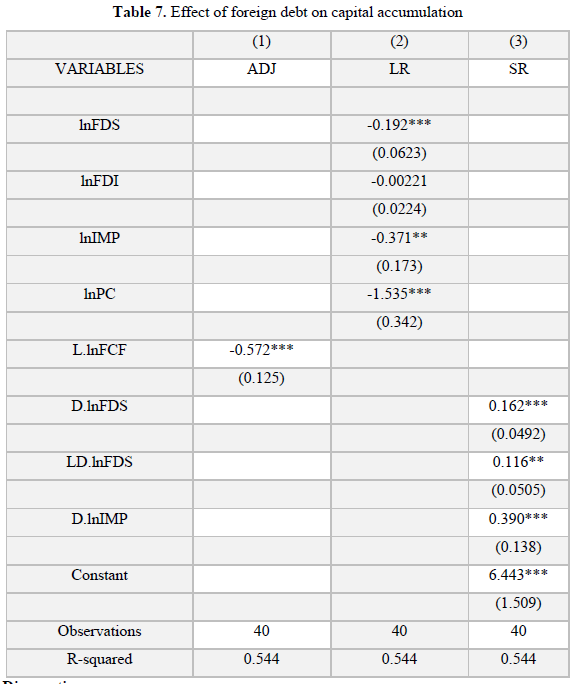

Regarding the effect of foreign debt servicing on capital accumulation, the results in table 7 show that a unit increase in debt servicing leads to a decline in capital accumulation by 3.1 units. This is indicated by the coefficient of foreign debt servicing that was found to be significant at 1%. Similarly, foreign direct investment, imports and household consumption expenditure have negative effect on capital accumulation. The effect is however, insignificant for the import variable. The outcome of the effect of foreign debt servicing on capital accumulation is consistent with the economic theory which asserts that increased borrowing and investing the borrowed funds in unproductive investment impacts the economy negatively. In the same vein, arise in consumption expenditure as opposed to development expenditure has a negative effect on the economy due to a decline in capital accumulation.

DISCUSSION OF THE RESULTS

The results in table 6 showed that in the short run, foreign borrowing is detrimental to domestic savings. The short run findings are similar to the theoretical postulation of Diamond (1965) who argued that high debt leads to increased taxes and hence savings. The results are also similar to the theoretical arguments of Barrell and Weale (2009) that debt servicing may reduce public investment-thereby impacting on private capital accumulation through complimentary effect on savings. The long run results, however, indicated that foreign borrowing has a positive effect on domestic savings. This outcome is contrary to the theoretical model that predicts that in the long run, foreign borrowing affects savings negatively. The long run results are also contrary to the empirical findings of Okafor and Tyrowicz (2009) who established that foreign debt had negative impact on domestic savings. However, the long run findings are similar to the empirical findings of Akram (2016) which indicated that foreign debt had a positive effect on domestic savings. regarding the effect of foreign debt on capital accumulation, the findings in table 7 showed that increased foreign borrowing is detrimental to capital accumulation. The findings are similar to Diamond (1965) who argued that a surge in foreign debt leads to a reduction in capital stock as a result of the substitution of government debt for physical capital in individuals’ portfolios.

CONCLUSION AND POLICY RECOMMENDATIONS

This study sought to determine theoretically the individual’s consumption and savings behavior amidst government foreign borrowing, and to analyze the effect of foreign borrowing on domestic savings and capital accumulation in Kenya. To achieve the objectives, a theoretical was developed involving a continuous two-period economy endowed with capital. The model is a two-stage game between the government's borrowing efforts and the representative household's adjustment of its savings effort. The model showed that in the long run the steady-state values of savings are positively related to output and negatively related to consumption, foreign borrowing, and debt service.

The empirical results indicated that, in the short run, foreign debt has a negative effect on domestic savings due to an increase in interest payment on debt. The long run results were, however, contrary to the theoretical prediction since the it was established that foreign debt has a positive effect on savings. This outcome would be the case if the funds borrowed externally was put into productive investment that generates sufficient returns to repay the debt and leave savings for the economy.

Regarding the effect of foreign debt capital accumulation, the study established that a rise in external debt causes a decline in capital accumulation. That is, increased borrowing accompanied by unproductive investment impacts negatively on the economy. Based on the findings, this study therefore, recommends a reduction in the external borrowing. This is poised to minimize the negative short run impact of debt in the economy through decreased savings. In the same vein, the study recommends debt to be used in productive investment to generate returns to repay the principle and the interest accrued thereby boosting economy-wide savings in the long run. A prudent use of debt would also boost the economy’s capital accumulation which is a catalyst for economic growth thus generating additional resources for debt repayment other development needs.

DISCLOSURE STATEMENT

There was no financial benefit provided to the authors to undertake the study.

No Files Found

Internationally Accepted

Share Your Publication :